Ontario Budget 2026: What the Proposed HST Relief Means for Home Buyers—and What Is Already Law

The Ontario government released its 2026 Budget today March 26, 2026, proposing significant new tax relief for home buyers. One of the most eye‑catching measures is a proposal to remove the full 13% Harmonized Sales Tax (HST) on eligible new homes in Ontario.

While this announcement is encouraging, it’s important to understand what is proposed versus what is already law—and which HST rebates are currently available to buyers.

Proposed Ontario HST Relief for New Home Buyers (Not Yet Law)

The 2026 Ontario Budget proposes to:

Remove the full 13% HST on eligible new homes valued up to $1 million, providing a maximum rebate of $130,000 per eligible buyer

Maintain partial relief for new homes valued up to $1.5 million

Work in partnership with the federal government, which has agreed to cost‑share by covering the 5% federal portion of the HST, subject to the passage of federal legislation

⚠️ Important caution

A budget reflects the government’s policy intention only. These proposed HST changes are not law until the required Ontario legislation is passed, and the federal government passes corresponding federal legislation for the GST portion. Home buyers should avoid relying on proposed measures until they are legally enacted.

What Is Already Law: First‑Time Home Buyers’ GST/HST Rebate (Received Royal Assent as of March 12, 2026)

Separate from the Ontario budget proposal, changes to the First‑Time Home Buyers’ (FTHB) GST/HST Rebate became law on March 12, 2026.

What is the First‑Time Home Buyers’ GST/HST Rebate?

This rebate is available to eligible individuals who are buying, building, or substantially renovating their first home.

The home must be:

Newly built or substantially renovated, and

Used as the individual’s primary place of residence

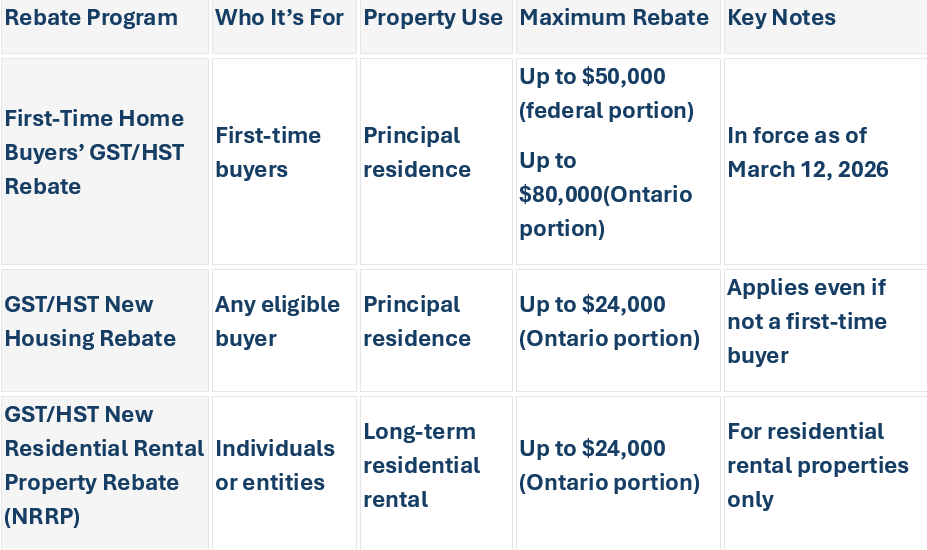

Depending on the value of the home, an individual may recover up to 100% of the GST (or the federal portion of the HST), to a maximum of $50,000.

Rebate amounts based on home value

$1 million or less → up to 100% rebate (maximum $50,000)

Between $1 million and $1.5 million → rebate is gradually reduced

$1.5 million or more → no rebate

Who Can Apply?

You may qualify if:

You are a first‑time home buyer

You intend to occupy the home as your principal residence

You purchased or built a new home

The agreement of purchase and sale was entered into on or after March 20, 2025 and before 2031

All other conditions are met

When Do You Apply?

You have up to two years from the date ownership is transferred to submit your rebate application.

What If You Don’t Qualify as a First‑Time Buyer?

Not qualifying for the first‑time home buyer rebate does not automatically disqualify youfrom other GST/HST relief. Depending on how the property is used, you may still be eligible for:

The existing GST/HST New Housing Rebate, or

A GST/HST New Residential Rental Property Rebate

Overview: GST/HST Housing Rebate Programs (Simple Comparison: Assume an induvial purchased a $1M house located in Ontario)

Final Thoughts

The proposed Ontario HST relief could be a game‑changer for future home buyers, but it is not yet law. In contrast, the first‑time home buyer GST/HST rebate enhancements are already in effect, and existing housing rebates remain available depending on how the property is used.

Before making decisions or signing agreements, buyers should understand which rebates currently apply and monitor legislative developments closely.

If you have questions about how these rebates apply to your specific situation—whether you are buying to live in or to rent out—professional advice can help ensure nothing is missed.

CRA Resource: GST/HST new housing rebate - Canada.ca

First-time home buyers’ (FTHB) GST/HST rebate

GST/HST new residential rental property rebate

Disclaimer

The information above is based on the Income Tax Act and CRA administrative guidance available as of March 26, 2026. It is provided for general informational purposes only and does not constitute tax, legal, or accounting advice. Individual situations vary, and tax rules can be complex. Please consult a qualified tax professional for advice tailored to your specific circumstances.